Would you pay ten times your yearly salary for a plant that will most likely die in about a week? Does paying $300,000 for a tulip seem like too much? In this post we will briefly explore arguably the first recorded economic bubble.

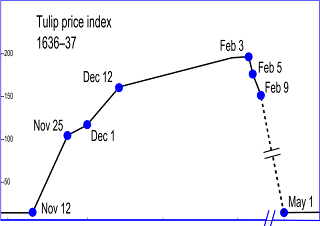

First a little background: Tulip mania or tulipomania was a period in the Dutch golden age when tulips were trading at extraordinarily high levels and then suddenly collapsed. In 1637 some tulips were trading at up to 10x times the annual income of a skilled craftsman. After the tulip was introduced by the Ottoman Empire in the mid-16th century, it quickly became a status symbol and desired by all. Tulips, which grow from bulbs, can only be uprooted and moved from about June to September and actual purchases of tulips would occur during these months. During the rest of the year traders would sign contracts to purchase tulips at the end of the season, thus the Dutch effectively created the first futures contract as a product of the market for durable tulip bulbs.

Interestingly enough, the Dutch also developed the concept of “shorting” the tulip market, which, simply put, means if the value of the tulip goes down, the purchaser of the short makes more money, and likewise if the value goes up, the purchaser of the short loses money (a practice quickly banned by the government but legal today).

People were purchasing bulbs at higher and higher prices, intending to resell them for a profit; however this scheme could not last unless someone was ultimately willing to pay such a high price. When speculators could no longer find someone to buy at the inflated price, demand began to collapse and prices plummeted as the speculative bubble began to burst. Some found themselves holding a contract to purchase tulip bulbs at ten times their market value and others found themselves in possession of bulbs worth just a fraction of the price they had paid.

How could individuals and society as a whole become so enamored with tulips that they were willing to pay astronomical prices compared to the intrinsic value of the bulb itself? Could people have been so foolish back then?

While the exact cause of the rise, and dramatic fall of the tulip prices during the late 1630’s is contested, partly because of the lack of accurate bookkeeping during the time, one suggested cause is still seen today: Social mania, which leads to the boom and bust cycles we see in the stock market today, such as the dot-com bubble and the housing bubble.

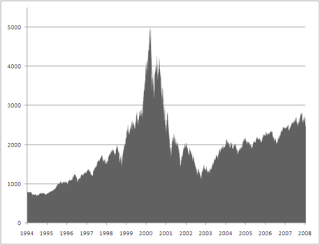

The dot-com bubble from 1995-2001 ended on march 10th 2000 with a NASDAQ peeking at 5,132.52. (For reference, it is about 2,830 as of today) During this period, investors who were just beginning to understand the monetization capability of the internet, invested large amounts of money in companies which were producing large annual losses. It was dot-com theory at the time for an internet company to expand its customer base as rapidly as possible even if it produced large annual losses. “Get large or get lost” was the wisdom of the day. At the height of the dot-com bubble it was possible for a promising dot-com to make an IPO of its stock and raise a substantial amount of money even though it had never made a profit, or earned any revenue.

When the bubble burst, fortunes were lost. As the NASDAQ lost more value, more people sold, which caused further losses and further selling; a pattern that continued on for some time until the rational market determined a truly fair price to pay for shares of dot-coms.

While not all dot-coms went bankrupt, as some were purchased by other companies, and some remain today, many fell in to the same pattern we saw almost 400 years ago. E.Digital Corporation for example traded for $2.91 on December 31st 1999 and quickly rose to $24.50 on January 24th 2000 less than a month later. As the bubble burst it fell to between $0.07 and $0.16 per share losing about 99.4% of its value in a few weeks. Could we really have valued shares at over 150x their market value and fallen victim to the same boom and bust seen with tulips?

The idea that the boom and bust cycle is a thing of the past and won’t happen again is a false assumption. It’s nearly impossible to see the see the bubble while you’re in it, and even harder to time the market. There will be more bubbles and more fortunes lost, as the short term value of an asset is still driven by investors, who have emotions and are human. Be wary when buying tulips, or flipping a house, or starting a dot-com seems to be the “investment of the week,” you may find yourself holding a valueless tulip bulb you overpaid for, even if everyone promised that “This time it’s different.”